The perfect storm battering the UK’s construction industry has sent claims costs soaring and vastly increased the risk of insureds finding themselves with a liability limit shortfall. The first instalment of this three-part series examines how construction claims inflation is threatening liability limits.

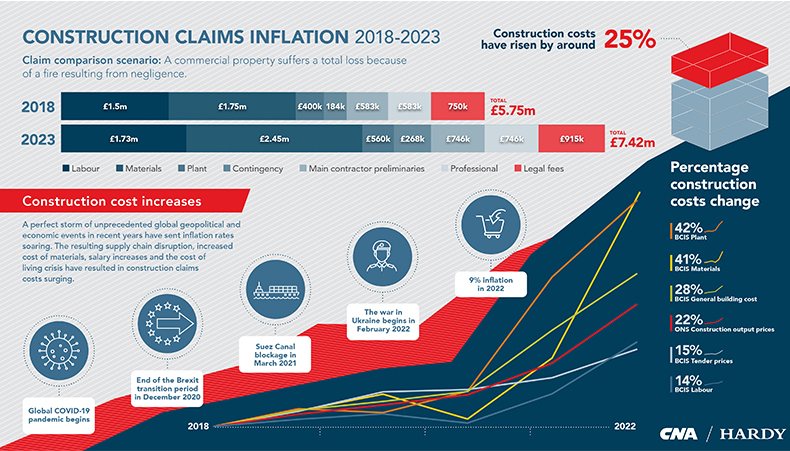

The Covid pandemic, the end of the Brexit transition period almost three years ago, the Suez Canal blockage in March 2021, and the war in Ukraine since February 2022, have led to serious shortages of materials including steel, timber, bricks and cement. The impact of the events now unfolding in Israel and Gaza is as yet unclear but further disruption to shipping schedules and supply-chain bottlenecks look likely.

All this has led to multiple collapses among homebuilders and an inflationary spiral that has included a 14% hike in labour costs and 41% rise in material costs. The result is significant claims inflation, with a like-for-like claim costing £5.75m in 2018 compared to £7.42m in 2023, as show in the graphic below.i

This rise in claims costs makes it all too easy to breach insurance limits, which can be detrimental to an insured’s livelihood.

The biggest threats to liability limits and who is at risk

Standard liability limits are typically between £1m and £10m under a primary public liability policy and the mandatory £5m or £10m under primary employers’ liability cover. The most likely type of damages to breach these limits are:

- Property damage, including a decrease in value and the costs of repair and the related economic loss

- Business interruption

- Delay/prolongation costs

- Costs incurred in mitigating the loss

- Alternative accommodation or premises.

The leading causes of such damages in the UK are fire (24%), building collapse (24%) and other factors including water damage, personal injury and environmental damage.ii

Some of the types of customers most at risk of breaching standard liability limits are contractors, subcontractors, manufacturers and suppliers of goods.

What does this mean in practice? Exploring a real-life claims example

The insured in our case study is a coffee machine maintenance contractor with £5m public liability cover for any one occurrence, with an excess of £10,000 on the same basis.

At first sight that limit seems reasonable – how risky can repairing coffee machines be?

A fast-food chain, McDougalls, calls the contractor in when a machine in a shopping centre-located restaurant develops a fault. The insured services the machine for a fee of £300 plus VAT but when replacing a component part, it makes a poorly formed electrical connection which ultimately causes the machine to ignite. The ensuing fire damages not only the McDougalls restaurant but other restaurants and shops within the shopping centre.

Multiple claims are brought against the insured from owners of the damaged properties to the combined tune of £15m, including £6m for damage to buildings and loss of stock and £9m in business interruption, as well as interest and claimants’ costs.

This leaves the insured with a shortfall of more than £10m above its £5m limit of indemnity. It can’t pay this and is ultimately wound up.

How would Excess of Loss insurance benefitted the insured?

The moral of this tale is that excess of lossiii insurance would have avoided this situation.

If the insured had taken out an excess policy with £10m limit of indemnity in excess of £5m, instead of financial ruin they would have only been responsible for their £10k excess. The primary insurer would have paid £5m in excess of £10k and the excess insurer would have covered £9.99m in excess of £5,010m.

Ultimately, the complexity of the average construction project means a lot can go wrong. Firms can easily find themselves exposed to the actions of third parties and have only limited oversight of what subcontractors and sub-subcontractors are doing.

The changing risk landscape, high claims costs and an unclear building-materials inflation and labour-market cost outlook mean it really pays to assume the very worst could happen. Claims inflation means that now more than ever it’s essential to review limits of indemnity and ensure that these are fit for purpose.

CNA Hardy’s excess of loss platform gives brokers and their clients the ability to quickly and easily add more limit, creating certainty in a highly uncertain environment.

About the Authors – Niala Butt & Justin Godman

Niala joined CNA Hardy in 2022 as Claims Manager - Casualty and Life Science, UK and Continental Europe. Niala is an Associate of the Chartered Insurance Institute and Chartered Insurer, she has significant Claims, Operations, Underwriting and Regulatory experience. Niala has specialised in complex catastrophic injury and Medical Malpractice claims across the UK and overseas jurisdictions, sitting on Government working parties, advising the Department of Health on lower value claims schemes and has an interest in inclusion, risk management and claims efficiency.

Justin joined CNA Hardy in 2012 and is Class Manager, Casualty. He is responsible for the strategy, portfolio management and performance of CNA Hardy’s Casualty business in the UK and Europe. Prior to joining CNA Hardy, Justin spent over 20 years at Zurich, Allianz and AIG in a range of underwriting and management roles. Justin is a Chartered Insurer and ACII qualified.

The information contained in this document does not represent a complete analysis of the topics presented and is provided for information purposes only. It is not intended as legal advice and no responsibility can be accepted by CNA Hardy for any reliance placed upon it. Legal advice should always be obtained before applying any information to the particular circumstances. Please remember that only the relevant insurance policy can provide the actual terms, coverages, amounts, conditions and exclusions for an insured. All products may not be available in all countries. CNA Hardy is a trading name of CNA Insurance Company Limited (“CICL”, company registration number 950) and/or Hardy (Underwriting Agencies) Limited (“HUAL”, company registration number 1264271) and/or CNA Services (UK) Limited (“CNASL”, company registration number 8836589) and/or CNA Hardy International Services Limited (“CHISL”, company registration number 9849484) and/or CNA Insurance Company (Europe) S.A., UK Branch (“CICE UK”, company registration number FC035780). CICL, HUAL and CICE UK are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority (firm reference numbers 202777, 204843 and 822283 respectively). The above entities are all registered in England with their registered office at 20 Fenchurch Street, London, EC3M 3BY. VAT number 667557779.

iBased on data from the Office of National Statistics (ONS) and the Building Cost Information Service (BCIS) including building, labour, materials and plant costs from 2018-2023. Legal fee estimates provided by DWF Adjusting Limited.

iiInsurer Claims Review 2022

iiiExcess of Loss insurance provides additional cover above a primary public liability policy and is an alternative to increasing the limit of indemnity. It is usually available when a primary insurer lacks capacity or appetite for additional cover.