Our previous Risk and Confidence research identified that global business leaders were becoming more attuned to the concept of reputation risk arising from corporate, compliance and supply chain exposures, and a variety of other drivers.

In response, we took soundings on reputation risk as a new risk category in our May ‘19 Risk and Confidence survey. The results are startling, as business leaders look ahead to May ‘20, we see that 29% of global business leaders predict their concern over reputation risk will increase.

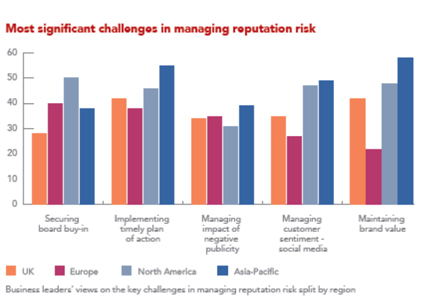

Reputation risk does not exist in a vacuum, it arises as a consequence of a misstep somewhere in the business – potentially a product failure, service shortfall, technology fault or an error of judgement by management leading to a governance failure. By its very nature, reputation is a risk that is deeply interconnected with the operation of the business itself and can effect organisations of all sizes.

How do we respond to reputational risk?

Insurers need to move to a new model: prevention and cure

In the past, insurers were called on to protect tangible assets: homes, buildings, employee liability and belongings. While that’s still very much the case, globalisation and the rise of the tech-enabled information economy mean insurance is also being called upon to protect more intangible things like cyber and data risk, trading relationships, supply chains, digital assets, intellectual property and reputation.

As tangible and intangible risks multiply; insurers, brokers and risk managers will need to work ever-more closely together to build appropriate resilience into business systems, processes and assets to better protect against interconnected risk and an increasing reliance on global trade and technology.

Reputation cover will become mainstream as boardroom risk is re-evaluated

Already we are finding significant appetite among our broker network and insureds for deeper discussion and insight around the drivers of boardroom risk and strategies for risk prevention and mitigation. In the same way the market has found a way to model the cost of non-physical damage business interruption claims as part of terror and political violence cover, we believe there will be appetite to model and mitigate the cost of managing reputation risk and the damage to brand value caused by specific triggers.

Interconnected risk will test management capability and organisational structures

Insurance managers, business continuity managers, security managers, health and safety managers, the risk financing team and the C-Suite need to create a joined-up view of the business, a cohesive 360-degree risk management strategy and an agile, rapid response to risk mitigation and control.

Global solutions will become increasingly sought after

Business today is becoming increasingly global, whatever the size of business. This means the insurance community will need to become more attuned to the challenges that raises in terms of politics, economics, supply chain, regulatory compliance and cyber threats that flow seamlessly through and across continents. This will mean much closer evaluation of the quality and efficacy of local partner networks, investment in higher quality partnerships and rapid adoption of technology-enabled solutions which will provide enhanced visibility, security and service.

Stuart Kenyon Head of Risk Control

Stuart Kenyon Head of Risk Control