Personal injury claims costs have surged since 2018, with more upward pressure expected in the months to come. The second instalment of this three-part series explores the impact of personal injury claims inflation on liability limits.

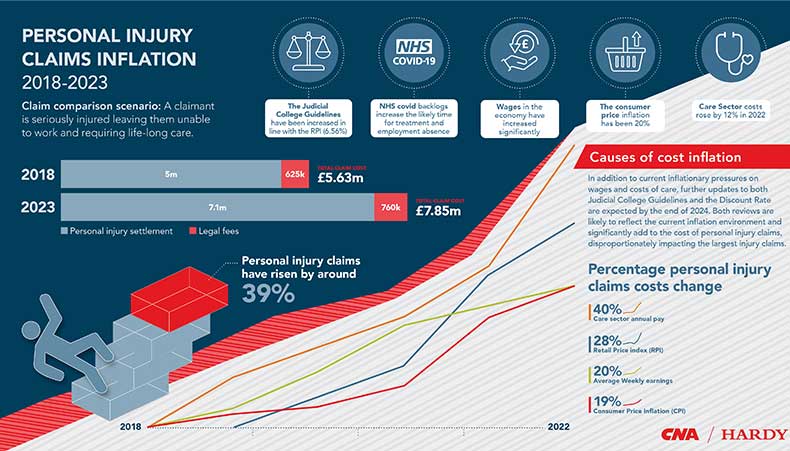

The graphic below shows how, in just five years, the cost of settling a personal injury claim has risen more than 39% - from £5.63m in 2018 to £7.85m in 2023.i

A 40% rise in care sector pay over the last five years as the industry battles to recruit and retain staff has pushed up long-term care costs. Average weekly earnings are up 20%, while the Retail Price Index, the higher of the UK’s two main methods of calculating inflation - and the one used by the Judicial College Guidelines for payout rates - is up 28%. The Consumer Price Index, the headline inflation gauge, is up 20%.

Factors expected to continue to force claims higher include NHS waiting lists, which increase treatment timescales and sick leave, as well as upcoming reviews of the Judicial College Guidelines for personal injury awards and the personal injury discount rate (PIDR) in England & Wales applicable to lump-sum compensation.

Demographic changes are also playing a part. With increased life expectancy, people are retiring later, meaning their loss of earnings in the event of an accident is greater. The cost of living crisis could impact claims frequency as accident victims become more inclined to seek recompense.

The biggest threats to personal injury liability limits and who is at risk

Calculating personal injury claims is complicated, time consuming and highly sensitive with some insureds and their insurers more likely to be exposed than others. Construction and related professions are particularly vulnerable, as are manufacturers and any business involving work from height.

Standard limits of indemnity under a primary public liability policy typically range from £1m to £10m while under an employers’ liability policy they tend to be £10m.

Among the losses that are most likely to breach these limits are:

- Accidents where there is a need for a care regime for life, given the rapidly rising cost of care, compounded by the NHS backlog.

- Accidents resulting in amputation generating losses above liability limits following huge advances in the technology used in prosthetics, and a related increase in their maintenance and replacement requirements.

- Accidents involving spinal cord and brain injury as these tend to result in complex care needs, lengthy rehabilitation, and either new accommodation or expensive adaptations to claimants’ existing homes.

- Claims involving nerve damage, chronic pain and severe fractures may also breach liability limits as these are heavily impacted by loss of earnings and pension benefits.

What does this mean in practice? Exploring a real-life claims example

Our case study, depicted in the graphic above, involves a claimant who is seriously injured following a workplace accident in 2018, leaving them unable to work and requiring life-long care.

The claimant issued proceedings against his employer and was awarded a personal injury settlement of £5m to cover care costs and future loss of earnings. This award, combined with £625k in legal fees, brought the total claims cost to £5.63m.

In 2018, this breached the insured’s liability limit of £5m and left them liable for £625k as they didn’t have excess of loss cover. While the insured may have survived this loss in 2018, the outcome today could well be different.

In the last five years, liability limits have remained constant however inflation has sent claims costs soaring. Should this same claim occur today, the insured would be liable for £2.85m - an increase of 2.23m – an amount which could easily result in the company’s bankruptcy.

The case serves as a poignant reminder of how easily personal injury claims costs can rack up and of the importance of brokers and insureds working together to ensure that liability limits are fit for purpose.

Our Excess of Loss e-trading platform, CNA Online gives brokers and their clients the ability to quickly and easily add more limit, creating certainty in a highly uncertain environment.

About the Authors – Niala Butt & Justin Godman

Niala joined CNA Hardy in 2022 as Claims Manager - Casualty and Life Science, UK and Continental Europe. Niala is an Associate of the Chartered Insurance Institute and Chartered Insurer, she has significant Claims, Operations, Underwriting and Regulatory experience. Niala has specialised in complex catastrophic injury and Medical Malpractice claims across the UK and overseas jurisdictions, sitting on Government working parties, advising the Department of Health on lower value claims schemes and has an interest in inclusion, risk management and claims efficiency.

Justin joined CNA Hardy in 2012 and is Class Manager, Casualty. He is responsible for the strategy, portfolio management and performance of CNA Hardy’s Casualty business in the UK and Europe. Prior to joining CNA Hardy, Justin spent over 20 years at Zurich, Allianz and AIG in a range of underwriting and management roles. Justin is a Chartered Insurer and ACII qualified.

The information contained in this document does not represent a complete analysis of the topics presented and is provided for information purposes only. It is not intended as legal advice and no responsibility can be accepted by CNA Hardy for any reliance placed upon it. Legal advice should always be obtained before applying any information to the particular circumstances. Please remember that only the relevant insurance policy can provide the actual terms, coverages, amounts, conditions and exclusions for an insured. All products may not be available in all countries. CNA Hardy is a trading name of CNA Insurance Company Limited (“CICL”, company registration number 950) and/or Hardy (Underwriting Agencies) Limited (“HUAL”, company registration number 1264271) and/or CNA Services (UK) Limited (“CNASL”, company registration number 8836589) and/or CNA Hardy International Services Limited (“CHISL”, company registration number 9849484) and/or CNA Insurance Company (Europe) S.A., UK Branch (“CICE UK”, company registration number FC035780). CICL, HUAL and CICE UK are authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority (firm reference numbers 202777, 204843 and 822283 respectively). The above entities are all registered in England with their registered office at 20 Fenchurch Street, London, EC3M 3BY. VAT number 667557779.

iBased on data from the Office of National Statistics (ONS) including Retail price index (RPI), Consumer price inflation (CPI), average weekly earnings, and care sector annual pay from 2018-2023. Legal fee estimates provided by DWF Adjusting Limited.