Economic and political risks are dominating the agenda within UK boardrooms. According to our Global Risk & Confidence Report, almost half (44%) of business leaders predict economic risk will rise through 2020 and 38% believe political risk will rise. The driver of course is Brexit.

The FTSE may be performing well, however as the value of the pound fluctuates, levels of anxiety within businesses are rising. As a consequence, confidence levels hit a new low in May this year with only a third of companies (36%) feeling confident in the ability of their business to grow and prosper, according to research conducted for our Global Risk & Confidence report.

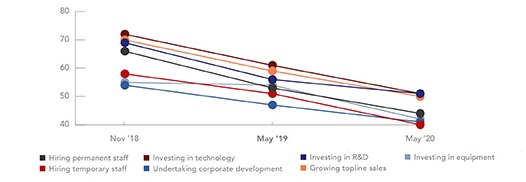

Our research shows that the lack of confidence is really evident in businesses’ spending plans, as investment in business fundamentals is down across the board.

Technology, R&D, corporate development, plant and equipment, talent – these are all fundamental aspects of a business’ operations that underpin its ability to deliver on the long-term business strategy. However, when the future is so unclear it’s a brave leader that is prepared to commit capital.

Investment in business fundamentals set to decline through to May 2020*

*(Taken from our Global Risk & Confidence Report)

Against this backdrop, it is perhaps not surprising that insurance rates are starting to rise. Brokers are being forced to invest in specialised training for those staff who have never experienced a hardening market in which insureds are actively worried about how the political and economic environment will impact on their business.

Businesses want protection

As insurers, the challenge we face is to craft an effective response to the risks that keep business owners awake at night. In our discussions with brokers and risk managers, we learn that businesses increasingly want protection against losses that traditional insurance policies are only just starting to cover, like loss of turnover, or damage to reputation that can flow from an adverse weather event, a warehouse fire, or Brexit itself.

The fire that started in an Ocado warehouse in February 2019 reportedly cost the company £110m and drove it to a £142.8m half-year loss, knocking 2% off its sales. When the so-called ‘Beast from the East’ hit the UK in spring last year, Debenhams reported a 1% fall in underlying sales due to reduced footfall and forced store closures, and the construction sector was said to have lost 1% (£1.6bn) of annual output. With traditional insurance, only the property damage caused by the warehouse fire would have been considered an insurable event.

In a similar vein, plenty of businesses are concerned by the impact of Brexit on their business – capital tied up in stockpiled materials; more expensive materials as a result of exchange rate shifts; and cash flow impacted by rising warehouse fees and weak sales.

The damage is likely to escalate further if we see a no-deal Brexit scenario under which businesses will have to come to grips with new trading arrangements, regulatory challenges and perhaps most significantly, the damage to reputation that will ensue if they are unable to meet the terms of their normal trading commitments.

How well is the industry responding?

Loss of profit and loss of attraction cover are starting to become more common and may include elements of brand or reputational damage. This approach has been pioneered in some food recall policies and by terror markets seeking to compensate businesses for non-physical business interruption losses – for example when access to premises is denied while investigations are carried out, or when footfall is reduced in the aftermath of an event.

Although there is no insurance market solution that could fully counter the business impact of a no-deal Brexit, it is encouraging to see that progress is being made in more general areas like loss of attraction and reputational damage. As the industry response shows, the answer to improving the management of complex and interconnected risks like these has to lie in building closer relationships and better dialogue with insureds.

As an industry, we may not have an answer to every problem, but we do have a strong track record of building solutions and working with brokers and clients to improve risk management, tailor risk transfer solutions, and boost the resilience which is needed when the economic and political backdrop puts businesses under stress.

Craig Bennett

Head of Casualty, International